Imagine a world where everything you perceive to be true about finance, family, fitness, food, etc… is not what millions of other humans perceive to be true. Not only that – people attempt to bring you down for your beliefs, or talk quietly amongst themselves about how stupid you are for doing the things you do. To be fair, you don’t think that highly of them either.

You’re experiencing selective distortion – welcome to planet Earth.

A Tale of Two Titans

Let’s take a look at two highly successful, well-respected financial gurus and their respective stances on debt:

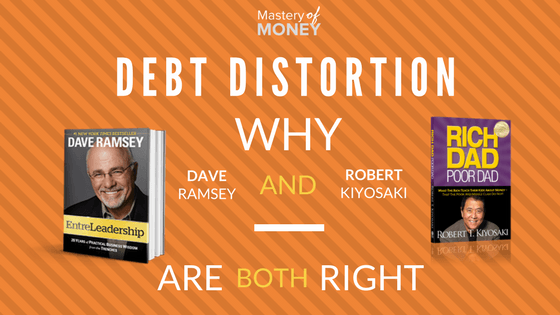

Robert Kiyosaki, author of Rich Dad, Poor Dad, says that there is such a thing as good debt – or debt used to buy money-generating assets like rental properties and business equipment.

Dave Ramsey, radio personality and author of The Total Money Makeover, teaches followers to avoid debt altogether, often quoting Proverbs 22:7 – “The rich rule over the poor, and the borrower is slave to the lender.”

Both agree that debt carried on credit cards and cars is to be avoided, because these things only make us poorer.

Kiyosaki is not against using credit cards persay, but teaches that balances should be paid in full every month.

While some see Ramsey’s stance on not using credit at all as extreme, the fact that the Federal Reserve estimates that almost half of U.S. households are unable to pay their credit card bills in full each month, and that these households owe more than $800 billion in card debt (about $15,000 per household), lends itself to the idea.

Ramsey proposes using mutual funds as a main investing vehicle for retirement, and is also a self-admitted lover of real estate as an investment, but only if one uses cash to purchase instead of mortgaging.

Kiyosaki advocates leveraging and using real estate as a primary builder of passive income and wealth.

Both programs have worked for millions of faithful followers. It would be easy enough to leave it at that, but sometimes in finance, just as in many other things, we tend to project what we know to be true on others. This is where things can get distorted.

Selective Distortion

When popular, polarizing methodologies exists – followers can come to believe that because it worked for them, their way is the only way and that people who follow other programs are therefore wrong, or worse – inferior. In marketing this experience is called selective distortion and, if left unchecked, the feeling can manifest itself into pride, anger, or even aggression. We’ve all seen this ugliness hiding in plain sight within comments sections of articles or blogs – in online forums, or even in our own personal circles.

As you have probably guessed, this same phenomenon occurs in religion, fitness, nutrition, and almost any other lifestyle category we can think of.

Back to our gurus – they get folks pointed down a path that inspires them to act and pursue their goals, and to be clear, most followers are not as dogmatic as described above. We use this example to illustrate the greater point: that sometimes no wrong choice exists.

Think about it this way- when it comes to deciding whether to follow Dave Ramsey or Robert Kiyosaki, here are a few of the primary options on the table:

- Dave Ramsey is right and Robert Kiyosaki is wrong.

- Robert Kiyosaki is right and Dave Ramsey is wrong.

- Both are wrong.

- Both are right.

Now, millions of people have had tremendous financial success following Ramsey’s program, so he’s obviously doing something right. The same can absolutely be said for Kiyosaki, so numbers one and two are out. If numbers one and two are out, then it follows that number three is also out. That leaves number four – they’re both right. Depending on how you define what is “right” for your financial goals, one may be “more right” than the other for you, and the other may be “more right” for someone else. Get it?

Stephen Covey stated “we must look at the lens through which we see the world, as well as the world we see, and that the lens itself shapes how we interpret the world.”

Our “lens” is a product of our years of experience, which equate to a sort of representational map of how we see the world. Your lens is so uniquely yours, how can any other human possibly share your exact views?

The short answer is that they can’t. This is why it’s not a loving venture to try and make them.

In what ways do you unconsciously or otherwise display selective distortion? Does it necessarily follow that what’s true for you must be true for everyone else? Is that line of thinking a burden we should even attempt to bare?

Putting the “Personal” in Personal Finance

When it comes to personal finance, is there a right or wrong way? Can solutions to life’s most complicated problems possibly be black and white?

Sure, there are basic financial tenets that every Ramsey, Kiyosaki, and Orman would agree on, like avoiding credit debt balances, getting your money to work for you, protecting against emergencies, etc…

But what about questions that are affected by individual discipline, knowledge, confidence, or risk-tolerance? Is every aspect of personal finance truly “one size fits all?”

- If you are knowledgeable about credit, and have the income to support paying off your credit balance each month to establish or maintain a score, should you still avoid using credit cards altogether because someone else told you so?

- If you have a very low risk-tolerance and experience emotional or physical anxiety about debt, does that mean that you are destined to be “poor” the rest of your life because you are unwilling to leverage yourself to purchase real estate?

The answer in both cases may be no, but ultimately it’s your personal decision to make. That’s why they call it “personal” finance.

Takeaways

Consider the following questions describing financial security from the Consumer Financial Protection Bureau:

- Am I in control of my day-to-day, month-to-month finances?

- Could I absorb an unexpected financial shock?

- Am I on track to meet my financial goals?

- Do I have the freedom to make choices that allow me to enjoy life?

Now- wouldn’t it be fair to say that one could follow Dave Ramsey or Robert Kiyosaki, or any number of proven financial programs out there and still be able to answer YES to any of these questions if they stick to the plan?

Do your homework, then use a financial program that works for you-give it your all. You can find success in almost any proven methodology. Celebrate with those that are using the same program, and do not judge others that are finding success with a program that’s not for you.

Remember, what’s right for one is not necessarily right for all.

Relieve yourself of the task of judging others – your load is heavy enough as it is.

Just do you.

Derek Brainard is a financial philosopher and money whiz who lives with his wife and ridiculously cute daughter in Syracuse, NY. His views on money, life, relationships and living exceptionally can be read at www.Level1Life.com. Derek is a direct descendant of Vikings and has the sword and shield to prove it.

I got this website from my pal who informed me on the topic of this web site and at the moment this time I am visiting this web page and reading very informative content at this place.

http://financehints.eu

Pretty no-nonsense, Derek. You make a good point that different folks have different priorities and perspectives. Ramsey is both unrealistic and behind the times – his success is due mainly to great marketing of his book and educational materials, not from the alleged wisdom contained within them. I won’t waste space here blowing up his assertions. Kiyosaki is much more on point though he, too, makes some occasionally silly assumptions. Bottom line, there’s a lot of so-called conventional wisdom out there that is damaging to many folks. An example is the ongoing message that personal finance must be kept simple. For some folks, perhaps that is true. But for many more capable, the more detailed they can engage with their financial situation, the more they can achieve. Carrying a half-dozen credit cards with varying cash rewards based on category is certainly more complicated, for example, but for the person willing to be organized and keep track of those benefits, the pay off is much, much higher. In many instances, simple is code for lazy. Thanks!!